Farmland During Uncertainty - We Have Seen This Before

Short term news headlines tend to use sensationalism and fear-mongering in an effort to grab your attention. The future is always uncertain. It’s important to consider historical context and long-term trends to think about the impact of various macro environments.

We like to talk about how farmland is boring. It’s arguably the original asset. Unlike many modern assets that derive value from abstract concepts (e.g., brand reputation, financial instruments), farmland has inherent value. It's a physical, tangible resource. Its fundamental value lies in its ability to produce something essential, regardless of economic fluctuations.

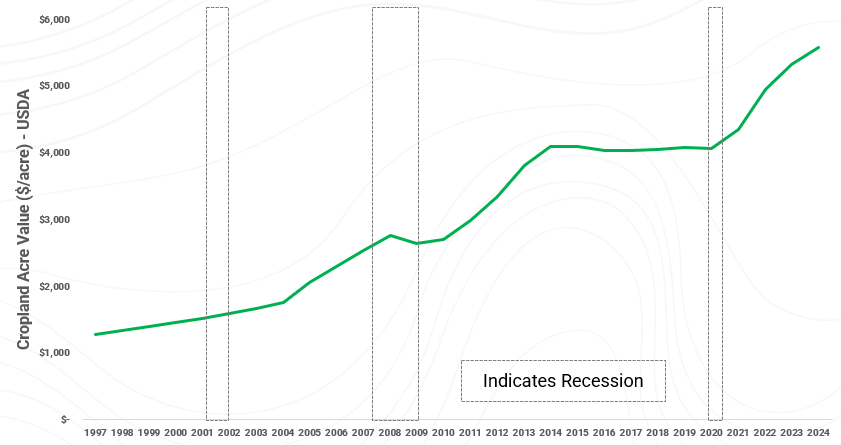

Farmland has historically proven itself to be a store of value during recessionary periods. In addition, we have seen the impact of tariffs and trade wars on farmland values before, as we have discussed in previous articles. Farmland, especially arable land suitable for agriculture, is a limited resource. It's not something that can be manufactured or easily expanded, which contributes to its inherent and long-term value. Increasing population and decreasing supply of arable land have contributed to a scarcity of investment quality farmland. We have discussed in detail in past articles how the scarcity of farmland impacts the capital cycle. Figure 1 below shows historical values of cropland in the United States, according to USDA data. Through multiple recessions, trade wars, political regimes, and geopolitical events, farmland values have remained resilient.

Figure 1 - Historical Cropland Values (Excludes Income from Farmland)

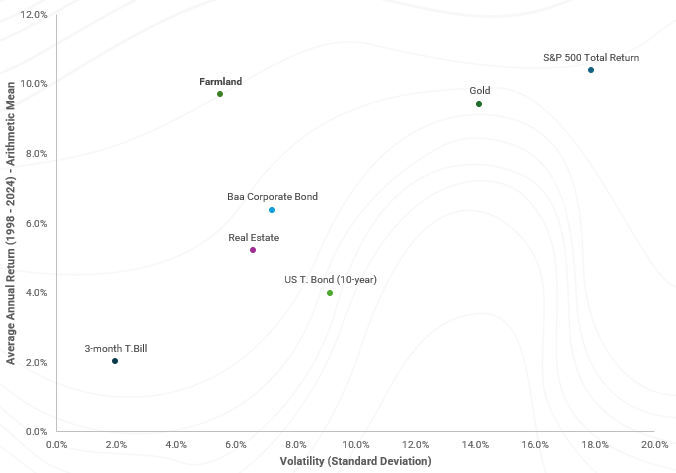

While farmland is not often considered as an asset class in the same way as stocks and bonds, its historical performance is worth consideration. The USDA has provided values and cash rent per acre for cropland (excluding improvements) since 1997. Figure 2 shows the average annual return of various asset classes, along with the standard deviation, or volatility of those returns. As the historical data shows, Farmland historically has demonstrated competitive returns with less volatility.

Figure 2 - Average Annual Returns vs. Volatility

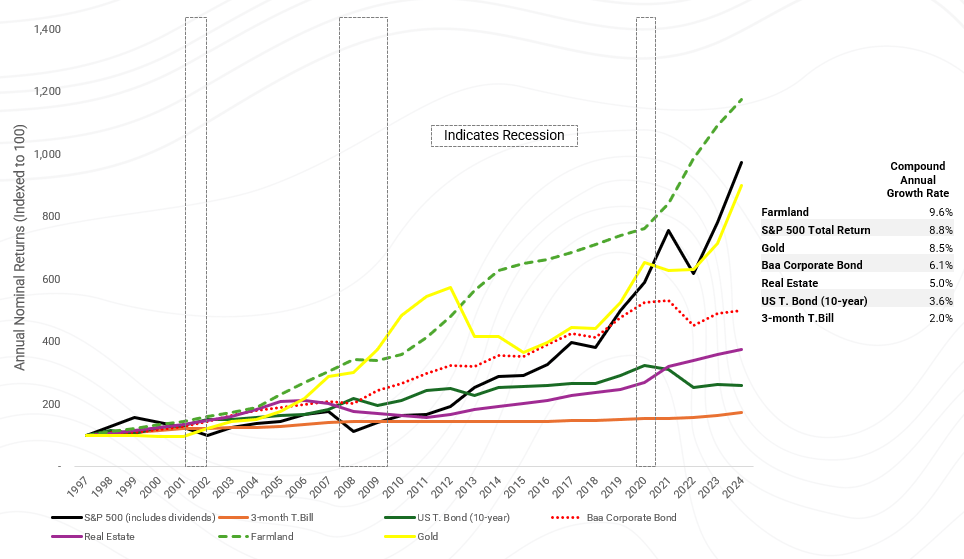

Figure 3 then shows the compounding effect of these returns over time for each asset class. Historically, farmland has shown the ability to generate returns competitive with stocks and gold, at a much lower level of annual volatility.

Figure 3 - Historical Nominal Total Returns of Various Asset Classes

The Importance of Inflation

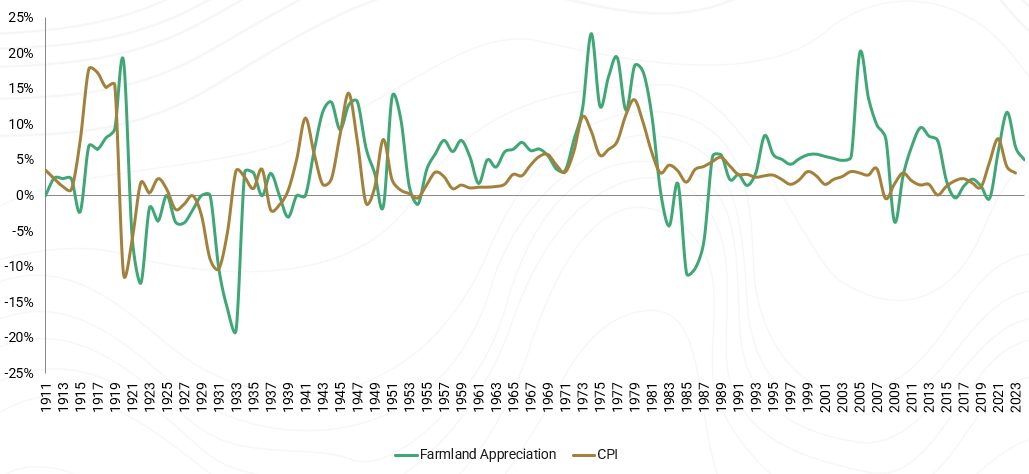

It’s also very important to consider the impact of inflation on various asset classes. Historically, farmland has a positive 0.67 correlation to inflation. Figure 3 below shows the annual change in farmland values, excluding any income from the land, compared to the CPI Index.

Figure 4 - Farmland Appreciation is Positively Correlated with Inflation

Farmland’s historical outperformance to yield-focused financial assets is more pronounced considering real returns, or the total return after inflation. This is one reason it is important to consider capital appreciation and not just yield when comparing various asset classes. The current yield on the 10 year treasury is ~4.2%. The latest CPI report from the Bureau of Labor Statistics showed the CPI increased 3% over the last 12 months. That would put the real yield at approximately 1.2%. Inflation erodes the purchasing power of a bond. For example, a $1,000 bond with inflation running 3% a year, will be worth approx. $970.87 the following year. This impact only compounds over time.

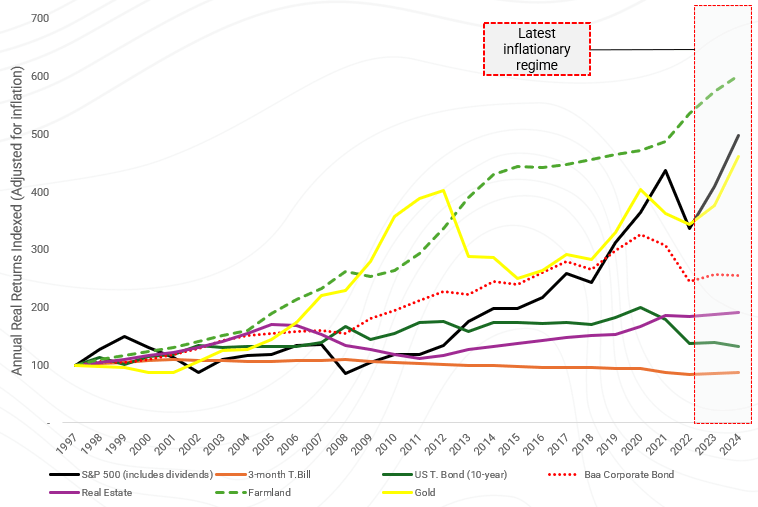

Conversely, farmland values historically have been positively correlated with inflation and have shown a positive spread to inflation. The historical average spread is 1.16% dating back to 1911. So historically, when inflation rises, farmland values rise to a greater degree. This has been the primary driver to the relative real return outperformance of farmland shown in Figure 5.

Figure 5 - Annual Real Returns of Various Asset Classes

Farmland: The Original, Boring Alternative Asset

While alternative investments are seeing increased investor allocations recently, farmland is not commonly found in investment portfolios due to the historical difficulty in accessing the asset class. Over the last 7 years, AcreTrader has worked to democratize access to farmland and while we have made significant progress, we still have a very long way to go.

Disclosures and Index Information

Past performance does not guarantee future results and there is no guarantee this trend will continue. All returns are estimates and assume reinvestment of dividends. Index information is provided for illustrative purposes only and is not meant to represent the results of an actual investment. The historical performance of each index cited is provided to illustrate historical market trends and not an individual property, fixed income instrument, or stock.

Farmland Return Data USDA data is based on USDA enumerators sampling of multiple parcels in each given region and therefore represents a diversified proxy of the overall market. Farmland investments on the AcreTrader platform are held in single-asset entities and therefore lack the diversification of an index. You cannot invest directly in a farmland index or in the properties represented in the USDA data. Farmland Total Returns represent annual farmland appreciation and annual cash rent per acre. Returns do not include any management fees, transaction costs or expenses. Asset Class References from Aswath Damodaran:

S&P 500 - Mr. Damodaran uses the S&P 500, which was created in 1957, and then back fills the data using other indices of large market cap companies that existed prior. Each year, he computes the annual return, by first computing the dividend yield by dividing the dividends paid and the price change in the index, by the level of the index at the start of the year. Thus, if the index starts at 1000, and increases to 1080, while delivering a dividend of 5, Mr. Damodaran’s annual return = (1080-1000+5)/1000 = 8.5%

US T. Bond (10-Year) - Mr. Damodaran uses the 10-year US treasury bond, since it is the only longer maturity bond with an uninterrupted history going back in time. For the data, he uses the yields on a constant-maturity 10-year bond, which can be found on FRED (the Federal Reserve website). Mr. Damodaran converts the yield into a return, by repricing the bond, issued at par at the prior year's yield, with the new yield, while keeping the maturity constant at 10 years. Thus, if the yield goes from 2.5% to 3%, he first prices a 2.5%, 10 year coupon bond with a 3% interest rate, and subtract this number from the par value of the bond which is $1000. That gives him the price change. Adding the 3% coupon for the current year gives Mr. Damodaran the total return.

US T Bill - Mr. Damodaran uses the 3-month US treasury bill, again choosing it over the 6-month because of longevity.

AAA & Baa Corporate Bond - Mr. Damodaran obtains the yield on a Moody's Aaa and Baa corporate bond yields from FRED and then computes the return on the bond, using the same approach that he uses for the US T.Bond.

Real Estate - Mr. Damodaran uses the home price data that Robert Shiller reports on his webpage to compute a real estate return on residential real estate. That series has now morphed into the Case-Shiller Index. Note that this return is just price appreciation, and will understate the returns on real estate by the cash flow return (from rental income) each year.

Gold - Year-end prices for gold, per oz. LBMA Gold Prices.

General Disclosures

Risk/reward profile for each asset class varies significantly. Investment objectives for farmland, real estate, gold, and stocks typically include long-term capital appreciation and current income, while investment objectives for fixed income are generally focused on current income. For each index, returns do not include any management fees, transaction costs or expenses and are therefore directly comparable on an expense basis. While this is a comparison of broad indexes, it is important to note that farmland and real estate investments are generally highly illiquid and subject to potentially high transaction costs, while stocks, fixed income, and gold generally offer a high degree of liquidity. Finally, this is a comparison of broad indexes, which are not directly investable. Tax considerations, fees, and expenses for each individual investor will vary significantly and are not considered in this comparison.