Diversification & Stability with Real Assets: Farmland vs. Gold

With the recent volatility in both the stock and bond markets, investors are increasingly searching for investments that provide diversification and stability. Real assets can serve as a hedge for investors’ portfolios during periods of volatility and provide defense against the prospect of an impending recession. There are a wide range of real assets readily available for investors, but recently gold has emerged as the go-to real asset investment for investors, increasing 75% in the last 18 months. Similar to gold, real assets that are positively correlated to inflation, such as farmland, can serve as stable and defensive assets in times of uncertainty. Below we will discuss gold’s similarities to farmland, the historical performance of gold relative to farmland, and why investors should consider farmland as a vital component of a diversified portfolio.

Farmland vs Gold: Similarities and Differences

While gold and farmland are both considered real assets, offering a tangible store of value, they possess distinct characteristics that lead to both similarities and differences in their investment profiles and potential returns.

Similarities:

- Hedge Against Inflation: Both gold and farmland have historically served as a hedge against inflation. As the purchasing power of fiat currencies declines, the intrinsic value of these tangible assets tends to hold up or even increase. Since 1928, gold has had a correlation of 0.18 with inflation while farmland values are more strongly correlated with a correlation coefficient of 0.69.

- Diversification Benefits: Both asset classes can provide diversification benefits to a traditional portfolio of stocks and bonds due to their often low correlation with these financial assets. Both gold (-0.07) and farmland values (-0.10) share a negative correlation with the S&P 500 since 1928.

- Finite Supply: The supply of both gold and arable farmland is inherently limited. The amount of gold that can be mined is finite, and the amount of productive farmland is decreasing due to urbanization and environmental factors. Since 1992, the United States has lost approximately 6 acres of farmland each minute according to USDA estimates. This scarcity can contribute to each asset’s long-term value.

- Tangible Assets: Unlike traditional financial instruments such as stocks or bonds, both gold and farmland are physical assets that can be seen and touched.

Differences:

- Income Generation: A key difference lies in their ability to generate income. Farmland, through lease income and the production of crops, can generate a recurring income stream in the form of rent or profits from direct operations. Gold, on the other hand, is a non-yielding asset and does not produce any direct income. Its returns are solely based on price appreciation.

- Liquidity: Gold is generally considered more liquid than farmland. It can be bought and sold relatively easily on global markets. Farmland transactions, however, are often less frequent and may involve higher transaction costs and longer holding periods due to the complexities of real estate.

- Management and Operational Requirements: Investing in farmland often involves management responsibilities, such as property maintenance, tenant management, or direct involvement in farming operations. However, AcreTrader has streamlined this process for investors making farmland a truly passive investment. Gold investments, particularly through ETFs or physical bullion, typically require less active management.

The Historical Performance of Gold and Farmland

Historically, both gold and farmland have demonstrated their potential as valuable components of a diversified portfolio, offering distinct risk and return profiles.

Gold's performance has often been characterized by periods of significant price appreciation, particularly during times of economic uncertainty, financial crises, and high inflation. For instance, gold prices saw substantial increases during the global financial crisis of 2008-2009 and during periods of heightened geopolitical tensions. However, gold can also experience prolonged periods of little appreciation or even price declines, especially when risk appetite in the broader market is high and interest rates are rising. Over the long term, gold has generally preserved wealth and provided a hedge against currency debasement.

Farmland, on the other hand, has historically exhibited more stable and consistent returns, driven by both income from lease revenue or agricultural production and appreciation in land values. The demand for food is relatively inelastic, providing a fundamental underpinning for farmland values. Furthermore, farmland returns have often shown a low correlation with stock and bond market returns, enhancing its diversification benefits. While farmland may not experience the dramatic price surges that gold has historically, its long-term performance has been competitive on a risk-adjusted basis, with lower volatility.

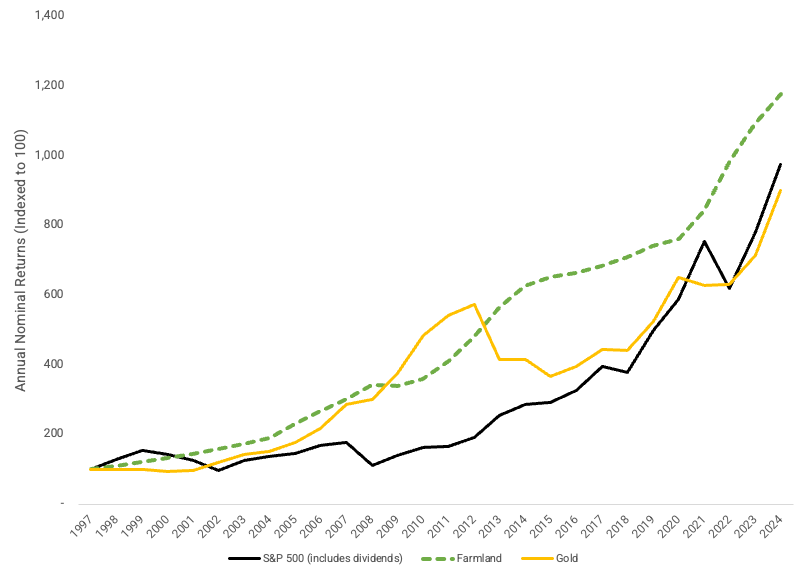

For a complete picture of historical farmland returns, it is important to incorporate data for both appreciation of the land and annual returns from rental income. The USDA has provided values and cash rent per acre for cropland (excluding improvements) since 1997. Figure 1 shows compounded nominal returns to $100 investment in gold, farmland, and the S&P 500 from 1997 through 2024. Across this period farmland outperformed both gold and the S&P 500 in total return while also exhibiting less volatility. Figure 2 shows the average annual return and volatility, represented by standard deviation of annual returns, for the three aforementioned assets classes.

Figure 1 - Historical Nominal Returns of Various Asset Classes

Figure 2 - Average Annual Returns vs. Volatility

In conclusion, both gold and farmland offer unique benefits as real assets in a diversified portfolio. Gold can act as a more liquid safe haven during times of uncertainty, while farmland has historically provided a less volatile, income-generating asset with strong long-term fundamentals. The optimal allocation to each asset class will depend on an investor's individual risk tolerance, investment horizon, and specific portfolio objectives. To see the farmland investment opportunities we currently have available, please check out our current offerings page.

Disclosures and Index Information

Past performance does not guarantee future results and there is no guarantee this trend will continue. All returns are estimates and assume reinvestment of dividends. Index information is provided for illustrative purposes only and is not meant to represent the results of an actual investment. The historical performance of each index cited is provided to illustrate historical market trends and not an individual property, fixed income instrument, or stock.

Farmland Return Data USDA data is based on USDA enumerators sampling of multiple parcels in each given region and therefore represents a diversified proxy of the overall market. Farmland investments on the AcreTrader platform are held in single-asset entities and therefore lack the diversification of an index. You cannot invest directly in a farmland index or in the properties represented in the USDA data. Farmland Total Returns represent annual farmland appreciation and annual cash rent per acre. Returns do not include any management fees, transaction costs or expenses.

Asset Class References from Aswath Damodaran:

S&P 500 - Mr. Damodaran uses the S&P 500, which was created in 1957, and then back fills the data using other indices of large market cap companies that existed prior. Each year, he computes the annual return, by first computing the dividend yield by dividing the dividends paid and the price change in the index, by the level of the index at the start of the year. Thus, if the index starts at 1000, and increases to 1080, while delivering a dividend of 5, Mr. Damodaran’s annual return = (1080-1000+5)/1000 = 8.5%

Gold - Year-end prices for gold, per oz. LBMA Gold Prices.

Risk/reward profile for each asset class varies significantly. Investment objectives for farmland, real estate, gold, and stocks typically include long-term capital appreciation and current income, while investment objectives for fixed income are generally focused on current income. For each index, returns do not include any management fees, transaction costs or expenses and are therefore directly comparable on an expense basis. While this is a comparison of broad indexes, it is important to note that farmland and real estate investments are generally highly illiquid and subject to potentially high transaction costs, while stocks, fixed income, and gold generally offer a high degree of liquidity. Finally, this is a comparison of broad indexes, which are not directly investable. Tax considerations, fees, and expenses for each individual investor will vary significantly and are not considered in this comparison.