The Difference Between Farmland Asset Values and the Agricultural Economy

What does [INSERT HYPERBOLIC HEADLINE HERE] mean for farmland values?

We are often asked, ‘what do higher/lower corn/soybean prices mean for farmland? How will higher input costs impact farmland values? How will tariffs or the OBBB impact farmland values?’ Many of these are headline grabbing events, and while we certainly track changes and the impacts to the agricultural economy, the ultimate answer is often, ‘historically not much.’

There is a fundamental disconnect in many investors' understanding when it comes to farmland as an asset class. Often investors' first thoughts of farmland are around changing commodity prices, input costs, or the agricultural economy overall. While these variables can have a marginal impact on farmland values, it is critical to differentiate farmland as an asset from the inevitable variability of the agricultural economy.

Historically farmland has not moved in concert with the inevitable swings in the agricultural economy. This is primarily due to the fact that farmland is not subject to the capital cycle that exists in many other asset classes. No amount of capital can increase the supply of high-quality farmland in the United States. Not only is farmland not subject to increases in the supply base, the supply of available farmland is steadily decreasing, with the U.S. losing approximately 4 acres every minute.

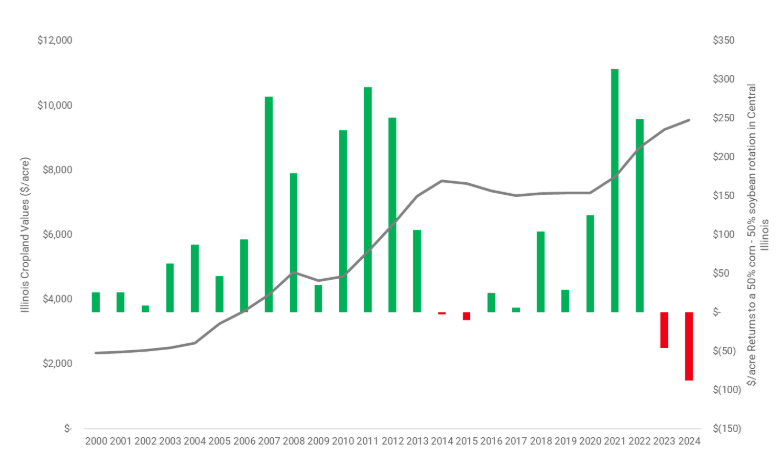

To test this, we can look at the historical data for one of the most homogenous(1) farmland markets in the country, Illinois. Figure 1 below shows Illinois cropland values (left hand side) vs. estimated $/acre returns for a 50% corn rotation, 50% soybean rotation in Central Illinois, according to Illinois FBFM and the University of Illinois. This brings all the variability of farming (commodity prices, weather, yields, crop insurance, input costs, overhead costs, etc) into an operator level return in terms of $ per acre.

Figure 1 - Illinois cropland values vs. $ / acre returns

While operator returns per acre exhibit significant volatility (standard deviation of 386%), cropland values in Illinois have been resilient, increasing at 6.1% on average annually with a standard deviation of just 7.3%.

Trying to apply changes in commodity prices to changes in farmland values has proven to be a fool's errand historically. If an investor were told in 2012 that corn prices would steadily drop -50% by 2017 and soybeans by -25%, an uninformed investor would think ‘surely farmland values will fall in Illinois.’ However, cropland values in Illinois increased by 14% over this time frame. And this says nothing of the annual income an investor would have received from lease payments each year.

The lack of correlation between operator returns and farmland values can be frustrating for analysts and investors. In practice, farmland shares similarities with other finite, real assets such as gold, silver, and fine art. Farmland also carries significant utility compared to these other real assets in providing the food, fuel, and fiber for the world. The limited and shrinking supply of farmland, coupled with the scarcity and competition for available farmland, has historically driven consistent farmland appreciation, even during times when commodity prices and operator returns are declining or negative. While other asset classes are exposed to the capital cycle, and thus increases in the supply base, farmland does not face this same risk.

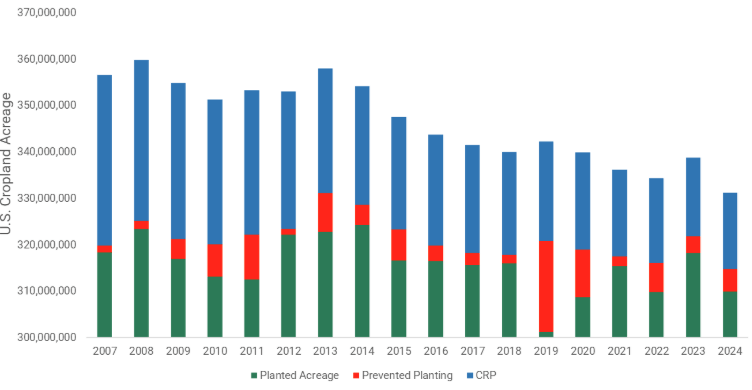

Figure 2 - United States Cropland Acreage

There is no doubt that the strength of the agricultural economy in any given region is important in understanding the long-term outlook for land values in that region. It is important to understand how long term changes in commodity prices, inputs, interest rates, and rules and regulations could impact land values on the margin. However, it is equally important to understand the framework that drives farmland asset values in each market. Periods of low operational returns have historically proven to be opportunities for long term investors who understand this framework. Farmers understand this framework best, as farmers are the primary purchasers of farmland, generally representing over 70% of farmland investments.

(1)To be clear, farmland is extremely heterogeneous, however on a relative basis, Illinois represents one of the most homogeneous.