What Drives Farmland Returns? Exploring the Evidence

Investors generally purchase stocks for potential capital appreciation and bonds and real estate for potential distribution income. It’s natural for many investors to try and place farmland into a context that is familiar, such as its distribution income, for comparison purposes. However, farmland carries different characteristics when compared to other types of real estate investments and therefore distribution income is only a minor contributor to potential total returns.

The key difference with row crop farmland when compared to other real estate investments is that it lacks meaningful improvements, and thus depreciating assets. There are no rental units that require maintenance or server racks that depreciate and must be replaced over time. Farmland represents an investment in productive soil and water rights that are well suited to produce certain crop types. We lose 4.8 acres of cropland every minute in the United States and no amount of capital can increase the supply of America’s farmland. Due to the shrinking supply of cropland and freshwater resources, farmland has historically appreciated in value, averaging 5.8% annually since 1997 according to the USDA. We believe that the key reason for investing in farmland is due to the potential for capital appreciation.

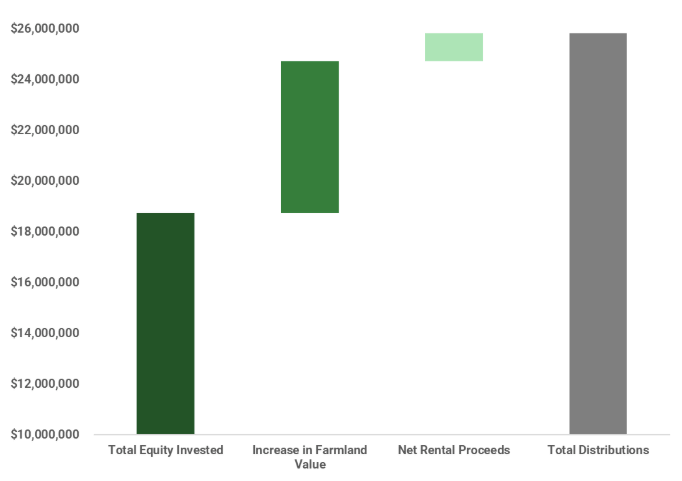

To best demonstrate this, we can point to our actual exits or realizations. AcreTrader Management has realized a total of 15 full cycle row crop farmland investments over the last 6 years. These exits represent approximately $18.75 million in equity invested and total returns of $25.8 million. The breakdown of these returns is presented below.

Figure 1 - AcreTrader Management Returns Waterfall

As shown, the vast majority of the return on equity invested, approximately 85%, was derived from the appreciation of the farmland during the hold period. The remaining 15% of the return on equity was derived from rental income. The total appreciation during the hold period across these 15 exits ranged from a low of 13% to a high of 88% with an average appreciation of 39%. The hold periods ranged from a low of 1.1 years to a high of 4.5 years with an average hold period of 2.6 years. The full list of exited investments is available here. As with all investments, past performance is not a guarantee of future results. Farmland investments carry the risk of geographic concentration, long-term volatility in commodity prices, weather events, and other operational factors. A full list of risk factors is available in the PPM for each offering.

While many real estate and fixed income investments are best suited for income-focused investors, we believe that farmland should be considered primarily for potential capital appreciation, in addition to income from distributions. For this reason, we prioritize purchase price relative to market value as the primary consideration in the farmland we acquire. Beyond purchase price relative to market, we then believe that the shrinking supply and scarcity of high-quality farmland presents an opportunity to identify a motivated buyer during the holding period to further drive returns for investors.